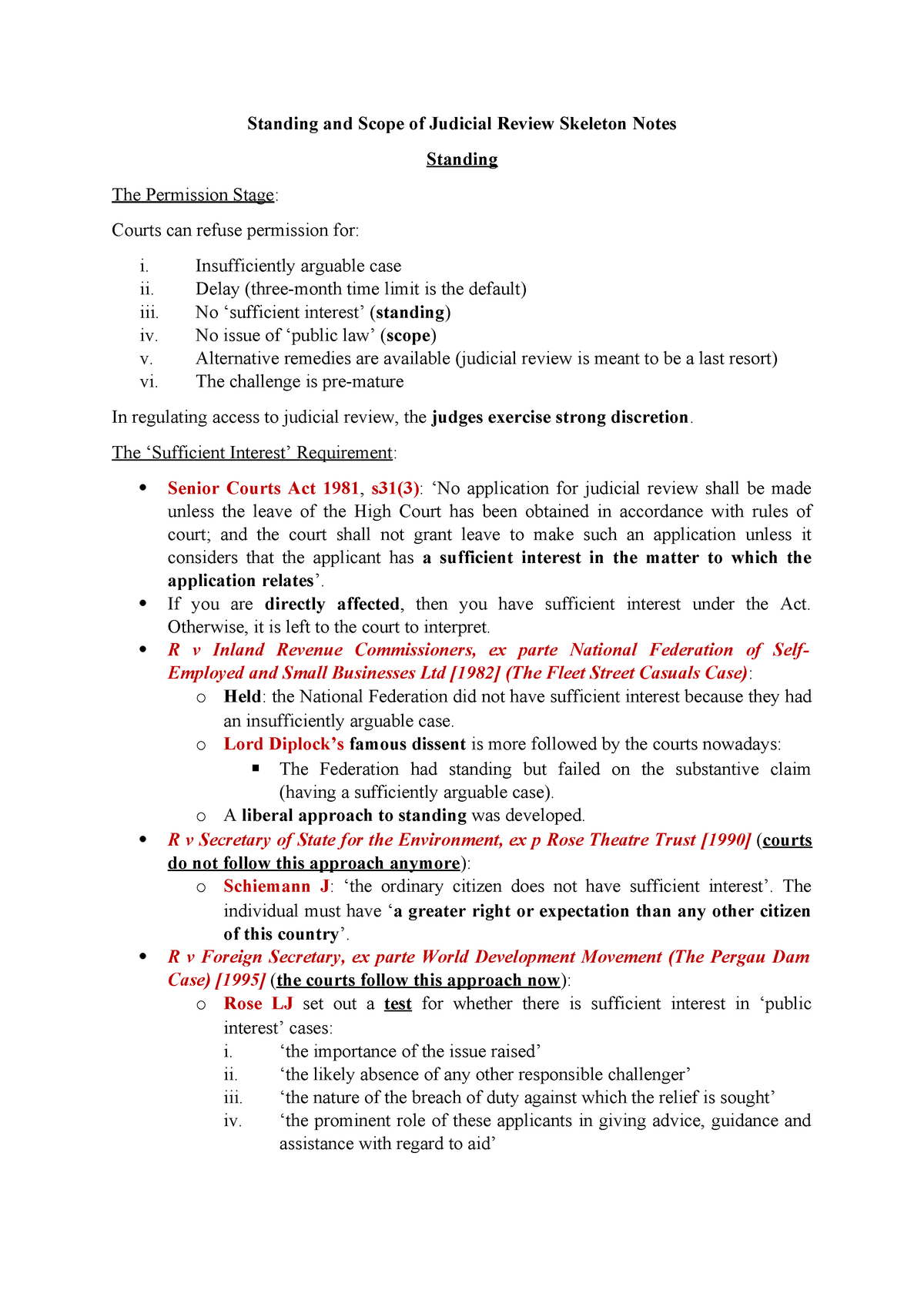

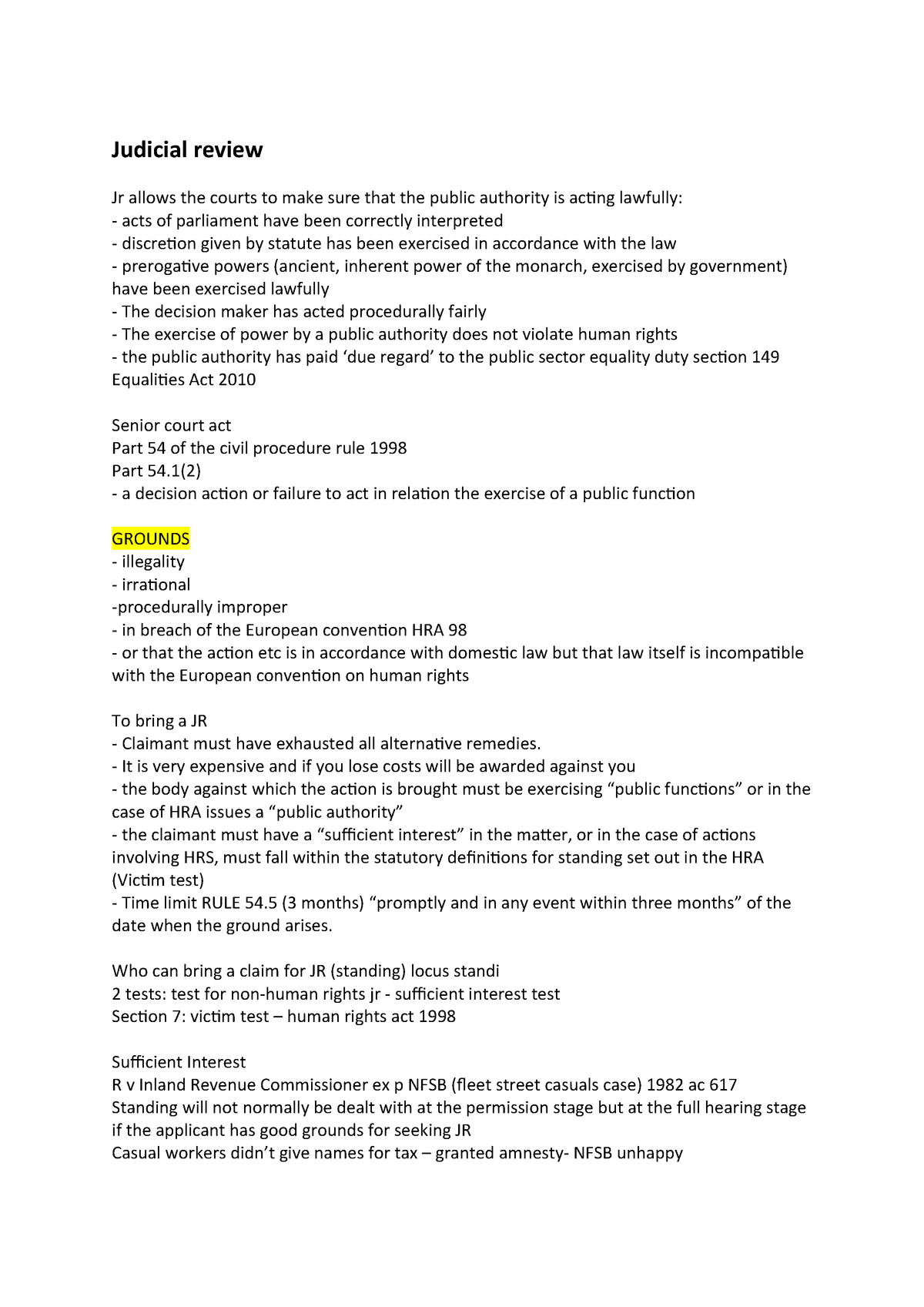

Fleet Street Casuals Judicial Review

Fleet street casuals case r v irc ex p national federation of self employed and small businesses 1982 ac 617 it involved a dispute about the taxation of casual print workers on national newspapers.

Fleet street casuals judicial review. However grounds such as irrationality come close to considering the decisions merits. A federation representing small businesses which had nothing to do with the fleet street casuals objected to the amnesty and sought judicial review. First important decision on the sufficiency of interest test casual labour was common on fleet street newspapers with the workers often adopting fictitious names. Key case r v inland revenue commissioners ex parte the national federation of self employed and small businesses ltd 1982 fleet street casuals federation sought to challenge the levy of taxes on casual workers engaged by fleet street.

R v inland revenue commissioners ex parte national federation of the self employed and small businesses ltd 1982 ac 617 house of lords also known as fleet street casuals chapter september. In an attempt to regularize the situation a deal was. Standing the fleet street casuals no busy bodies timely within 3 months ostler exhaustion of alternative remedies grounds can only review the legality of the decision not its merit. It was held on appeal that they did not have sufficient interest in the decision to grant an amnesty as they were no more than a interest group or body of taxpayers enquiring into the tax affairs of others.

A claimant for judicial review must have a sufficient interest in the subject matter. They avoided paying income tax by falsifying information provided to the tax authorities. Cited axa general insurance ltd and others v lord advocate and others scs 2010 gwd 7 118 2010 slt 179 scs bailii 2010 scotcs csoh 02 times 19 jan 10. A low threshold for standing in judicial review may be appropriate where there is no other way of holding the decision maker to account but where there are others who could bring judicial review it may be denied.

The charity had various subsidiaries conducting. It was held on appeal that they did not have sufficient interest in the decision to grant an amnesty as they were no more than a interest group or body of taxpayers enquiring into the tax affairs of others. It also sought judicial review of the decision of the tribunal not to allow it to raise an argument of legitimate expectation.

Judicial Review In Tax Cases At The High Court Legal Guidance

R National Federation Of Self Employed And Small Businesses Ltd

Ex Parte Dixon 1998

Public Interest Standing R V Sec Of State For Foreign Commonwealth

Http Heinonlinebackup Com Hol Cgi Bin Get Pdf Cgi Handle Hein Journals Manitob14 Section 17